Inflation: Reports of its re-birth are greatly exaggerated

Figure 1 Too much good news?

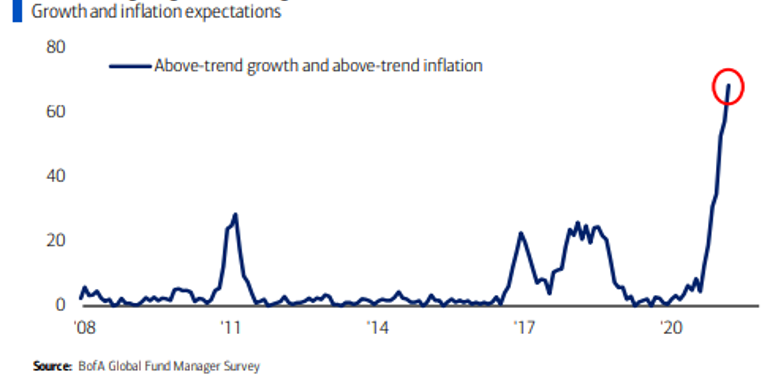

So much, actually too much, is being written on these topics and so, it behoves me to be forthright. It is perverse that many commentators often react as if good economic news is ‘bad’ and bad news ‘good’. Even worse, it is surely callous to die the proverbial thousand deaths over monetary policy when so many people really are dying and have yet to die from the pandemic. Nevertheless, commenting is what commentators do, just as burgling is what burglars do, while on the front line many traders and investors have never had to cope with inflation…..and .…..er……. without central bank largesse. Figure 1 from the May Bank of America Global Fund Managers Survey shows a record number of respondents expect an inflationary boom, relegating COVID-19 to a humble fourth place in the list of ‘tail risks’ (i.e. harmful).

Figure 2 Consumer Inflation in Developed Markets: cost-push has become less important

Source: Capital Economics

Inflation is here already

That is surely the easy bit to take on board. Commodity prices (notably building materials, industrial metals and many foods) together with those for oil and gas have been driving Producer Price Indices ever higher, especially on a year on year basis. This cost-push inflation has risen principally from supply chain disruptions because of the pandemic and also from the more recent renewal of the Russo-OPEC production pact. Figure 2 shows that the impact of food and energy on Consumer Prices has diminished in advanced economies but this is very much not the case in many developing economies. Not yet much in evidence is the demand-pull inflation that could arise from a ‘dam-burst’ in Consumption as pandemic restrictions are lifted but supply chain problems can be expected to be adding to the pressure on wholesale and retail prices. Indeed, Consumer Price Indices have risen sharply in the US since March and from April in the Euro Area (after 5 months of deflation in 2020), China and the UK, while they never really fell back in many developing economies (notably, India, Brazil, Mexico and South Africa). There is always the possibility of demand-pull inflation leading to higher wages while apparent labour shortages in the US are being seen as another major supply side challenge. It is still, however, rather difficult to interpret data which, due to the pandemic, is so affected by collection difficulties and also by comparisons with previous periods. For example, unfilled vacancies seem typically localised, as are redundancies while the labour force in the US and other advanced economies is less unionised than in the (cost-push) inflationary ‘70s and 80’s. There is certainly a long way to go in the US jobs market (Figure 3).

Figure 3 Not such good news after all!

What will limit the current ramping-up inflation (and growth) is a slowdown in demand and this was already in train before the pandemic broke. Consumption had for decades been increasing its share of economies around the world to around 70% in the US, 50- 60% in other advanced economies and variously less in developing countries. More recently, it has become clear that disparities in disposable income within and between counties have widened and the disruptions of the pandemic have further concentrated minds. Figure 4 shows the results of an IPSOS survey that posed a set of rather discomfiting questions to citizens in OECD member counties (plus Russia and Romania). Many will have suffered income and/or job losses or had family and friends who did so, will have read of the automation of white-collar (including professional) jobs and will be watching house prices running away from them. It is, of course, not all gloom and the scores from France and Italy are quite encouraging. Nevertheless, these are the responses of younger people who do not feel either able and/or willing to follow in the free-spending footsteps of their parents. New spending priorities and savings habits will have formed during the lockdowns, which suggests that any ‘dam burst’ will be rather more like sluice gates’ being opened rather too quickly. With the US leading the way, growth is bouncing back in the advanced economies and undeniably bringing inflation with it. However, COVID-19 is far from contained and more (genuinely) bad pandemic news can be expected out of Africa, South America, South/South East Asia and, whisper it softly, even in the richer countries.

Figure 4 Not such great expectations!

The pandemic is still here

This is most important! COVID-19 is out of control in India and parts of South America while new outbreaks are threatening some of the early success in Asia. The ‘Indian mutation’ is rampant in the UK. Vaccination rollouts are making a difference, practically and psychologically, but even in richer countries there remain the risks of new mutations and ‘vax hesitation’ limiting the level of herd immunity. There is plenty to hope for as governments, scientists and doctors around the world collaborate on devising the best combinations of lockdowns, vaccination, targeted restrictions and therapies. It may be possible by next year that governments will have decided to take their chance with lifting all restrictions that inhibit economic activity and downgrade COVID-19 to a pernicious form of ‘flu’ that everyone may get sooner or later. However, until such things are possible it is difficult to see the current growth in advanced economies as more than a bounce-back and the associated cost-push inflation as anything but temporary.

It should also be remembered that all was far from well economically before the pandemic struck. Some governments simply have more viable economies to (mis)manage while others have non-economic domestic priorities (e.g. China, Iran) that may hold back growth, both nationally and for companies that are deemed ‘systemic’. The Biden Administration has set a standard for post-pandemic recovery that every other government around the globe will be measured against, despite (because of?) many not actually sharing Mr Biden’s priorities on Climate Change and Poverty. As the US Federal budget deficit accelerates, some will look on enviously while feeling unable to fund fully their own recovery wish lists. Others may resort to outright money-printing, citing Modern Monetary Theory.

Accordingly, the central banks have a problem: they are deemed to be in charge of the economy and markets and expected to control them but in reality their power is much more limited. It seems that most, led by the Fed, would like to see higher interest rates and fewer asset purchases but they can only get there after issuing carefully worded forward guidance months in advance. They also feel obliged to support their governments’ fiscal stimulus by carrying on buying bonds. It has become very fashionable to accuse central bankers of being incompetent, reckless and deluded. More serious charges include corruption, conspiracy and….shock and horror……agents of communism or plutocracy or both. Somehow, it just seemseasier andsaferto believe what they are saying about inflation and rate hikes, even if one disagrees. Did someone say: ‘never fight the Fed’?

Figure 5 Keep panicking and carry on?