Beyond Brexit

I am going to resist writing either a review of ‘significant’ events in 2020 or ‘ten top predictions for 2021’. There are too many of those being aired already! I feel reasonably confident, however, in wishing readers a Happy New Year as 2021 will very probably be better for most of us and our businesses even if, alas, it also brings misery and misfortune to some. Even so, there are significant challenges, many directly and indirectly relating to the pandemic and which will go on well beyond the end of this year. Moreover, we have to remember that the global economy was not in great shape even before COVID-19 struck. Here, in the UK, we (including the Government itself) have still to work out what Brexit really means. Meanwhile, global equity markets have been enjoying the last few months, during which time it was quite difficult not to make rather a lot of money.

Figure 1 Global equity markets: better late than never?

On the ‘fantastic’ Brexit deal, on which far too much has already been written, I shall here confine myself to 4 observations:

A deal, any deal, was always inevitable as the potential economic disruption to both the UK and some Northern regions of the EU was too awful to contemplate. The uncertainty for businesses caused by the twists and turns of the negotiations, however, will have added to the structural damage from the UK’s giving up full membership of the Single Market and Customs Union.

The UK may, somewhat ironically, prove reluctant to push too far its new found freedom from EU laws and regulations, especially on environmental and employment matters, as it…er….actually agrees with most of them. State subsidies could cause more friction but EU governments will surely be just as keen as the UK to invest in ‘science and innovation’ while protecting existing jobs in more traditional sectors.

The dealing is far from finished as useful extra (air routes, driving licences and health cover) are already being added on a temporary basis with (surprise!) a good possibility of becoming permanent. Even the ‘Big One’ of financial and professional services recognition and access may start to be nibbled away…….and…..oh, yes…..the whole deal is subject to review in 5 years’ time!

Starting with the 2016 referendum itself, continuing through the tortured negotiations and now that many formal ties with the EU have ended, Brexit has been widening the political fissures within the UK, between and within each of the 4 ‘nations’ (especially England). Years of bitter and debilitating argument lie ahead, even if the union probably will hold in the end.

Figure 2 USD FX rates: pound wise or dollar foolish?

In the usual thin end of year trading it has been tempting to regard as the main stories Sterling’s strength and Bitcoin’s bonanza. However, even within those markets it is much more a tale of dollar weakness either through hedging or speculative shorting and this surely raises some rather important questions for the year ahead.

How much economic damage will the pandemic end up causing? Recovery as measured by GDP is already underway around the world but the outlook for Unemployment remains cloudy at best. There are high expectations for a post-vaccination release of pent-up demand for travel, leisure, hospitality and entertainment but that will depend, at least initially, on how many ‘suppliers’ are still in business. Meanwhile, buoyant retail sales suggest that consumers have not been holding back on buying ‘stuff’. There may be little doubt that the ‘haves’ outnumber the ‘have nots’ in the advanced economies but it seems unlikely that all of them will want to party in a new ‘Roaring Twenties’. Developing economies can be expected to outperform in GDP growth but, with the exception of China, miss out on the parties.

Are buoyant corporate earnings already priced in, especially in the US? There is no doubt that earnings will be higher for many companies and markets are always looking ahead. This may explain a sense of vertigo amongst some institutional investors and why they are starting to look outside the US while hedging their bets with the obvious pandemic ‘winners’ (Big Tech) and punting on new potential (mainly US) disrupters. This may explain why equities were up just about everywhere from November onwards and even why the USD fell from favour.

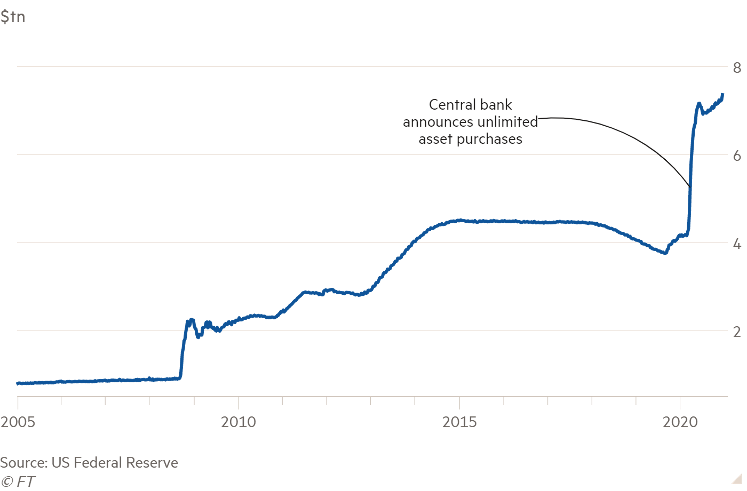

Can the Fed do much to alleviate the pandemic’s economic damage and hold up US equity prices? There is no doubt that the Fed would like to help on both fronts but it is showing signs of feeling constrained by the surge in the Federal US deficit and fear of the side-effects of negative official rates. The BoJ and ECB experiences seem neither effective nor reassuring on either count. Moreover, it does have to pay at least lip service to inflation and it has no defence should that take off soon. Any hint of rate hikes already causes US Treasury yields to shoot higher, as witnessed by some wild movements during Q4. Fortunately, inflation is likely remain subdued for the time being, although Oil prices have perked up and hedges in Gold are still firmly in place. Meanwhile, the Fed is unlikely to be troubled by dollar weakness against the pound or any other major currency but will surely be pondering the potential damage from the seemingly inevitable bursting of the Bitcoin bubble.

Figure 3 Never fight the Fed but what if it runs out of ammo?